Your Tax-Loss Harvesting Strategy Is Leaving Your Clients' Money on the Table

6 min read

|

April 16, 2026

200+ Basis Points of Tax Alpha Are Vanishing Between Your Reviews

Most advisors know tax-loss harvesting works. Fewer realize that when you harvest matters just as much as whether you harvest at all.

The difference between daily and annual harvesting isn't incremental. It's potentially 200+ basis points of tax alpha per year.1 Over a decade, that gap may compound into hundreds of thousands of dollars in after-tax wealth for your clients. And yet, the majority of the industry still harvests quarterly at best or outsources to ETFs that can only harvest at the fund level once a year.

That's not a rounding error. That's real money left on the table.

4x Your Tax Alpha with the Same Strategy

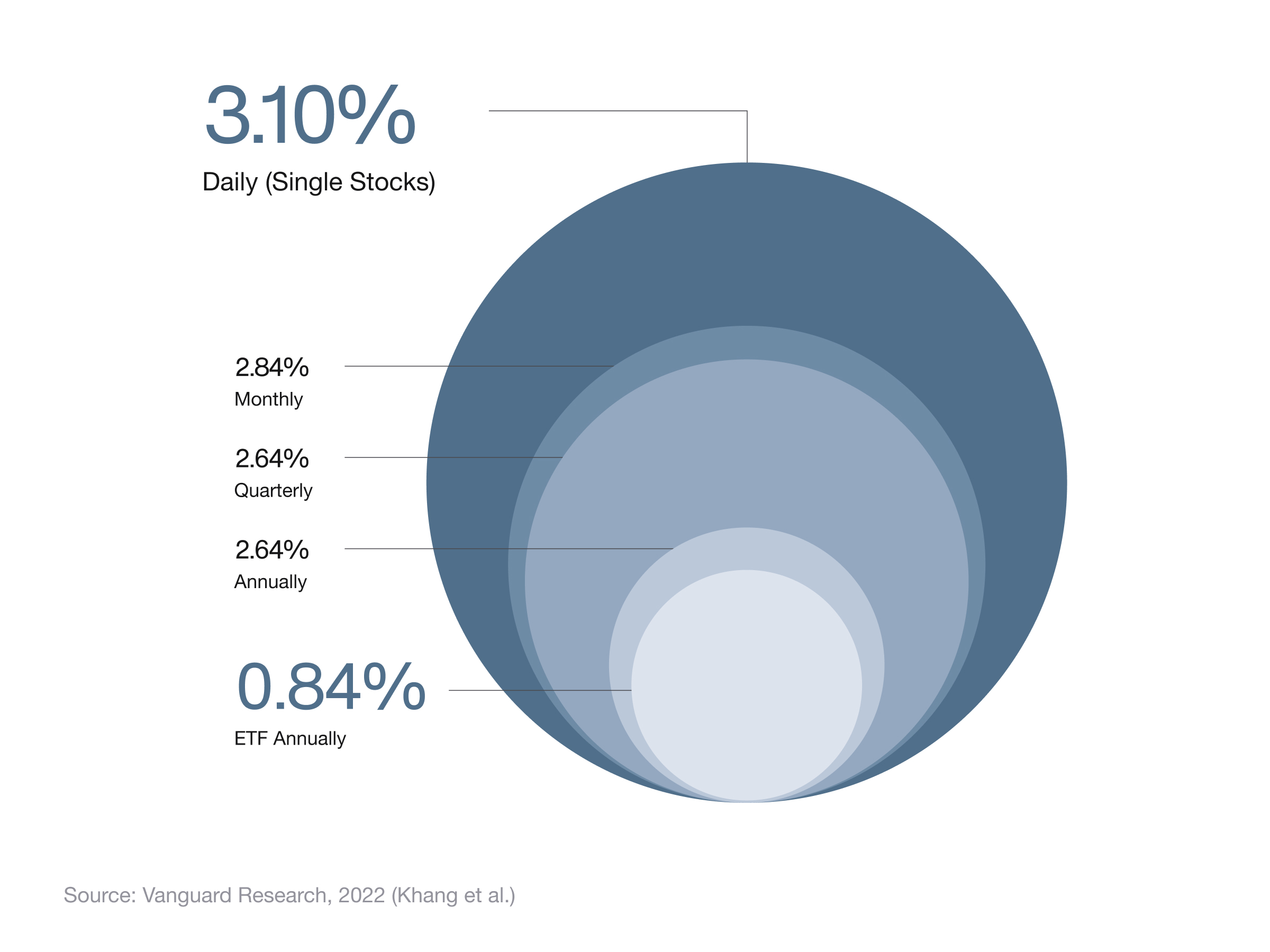

An advisor using annual ETF-level harvesting captures 0.84% in tax alpha. An advisor using daily single-stock harvesting captures 3.10%. That's nearly four times the tax alpha from the same underlying strategy, just by changing the frequency and the vehicle.1

The reason is straightforward. Markets move every day. Individual stocks within an index diverge constantly, even when the index itself is flat or rising. On any given day, dozens of positions in a diversified portfolio may be sitting at a loss, even in a bull market. If you're only looking quarterly or annually, those windows close before you ever act on them.

Daily harvesting captures opportunities that simply don't exist by the time a quarterly review rolls around.

No Advisor Has Time to Do This Manually. That's the Point.

At Vise, daily tax-loss harvesting isn't a calendar event. It's a continuous, automated process.

Our proprietary rebalancer and optimizer reviews every position in every portfolio, every single trading day. Harvesting is opportunistic, triggered by actual market movements rather than an arbitrary schedule. When a position hits a loss threshold, the system acts: it realizes the loss, replaces the position with a correlated holding to maintain exposure, and monitors wash sale rules automatically.

The result is a portfolio that stays aligned with its target benchmark while systematically capturing losses that a less frequent approach would miss entirely.

This matters because the mechanics of tax-loss harvesting are deceptively simple in theory but operationally intensive in practice. Doing it well at the individual stock level requires monitoring hundreds of positions simultaneously, tracking wash sales across accounts, maintaining sector and factor exposures, and minimizing tracking error. Doing that daily, across thousands of accounts, is an infrastructure problem, not a spreadsheet exercise, and infrastructure is what Vise was built to provide.

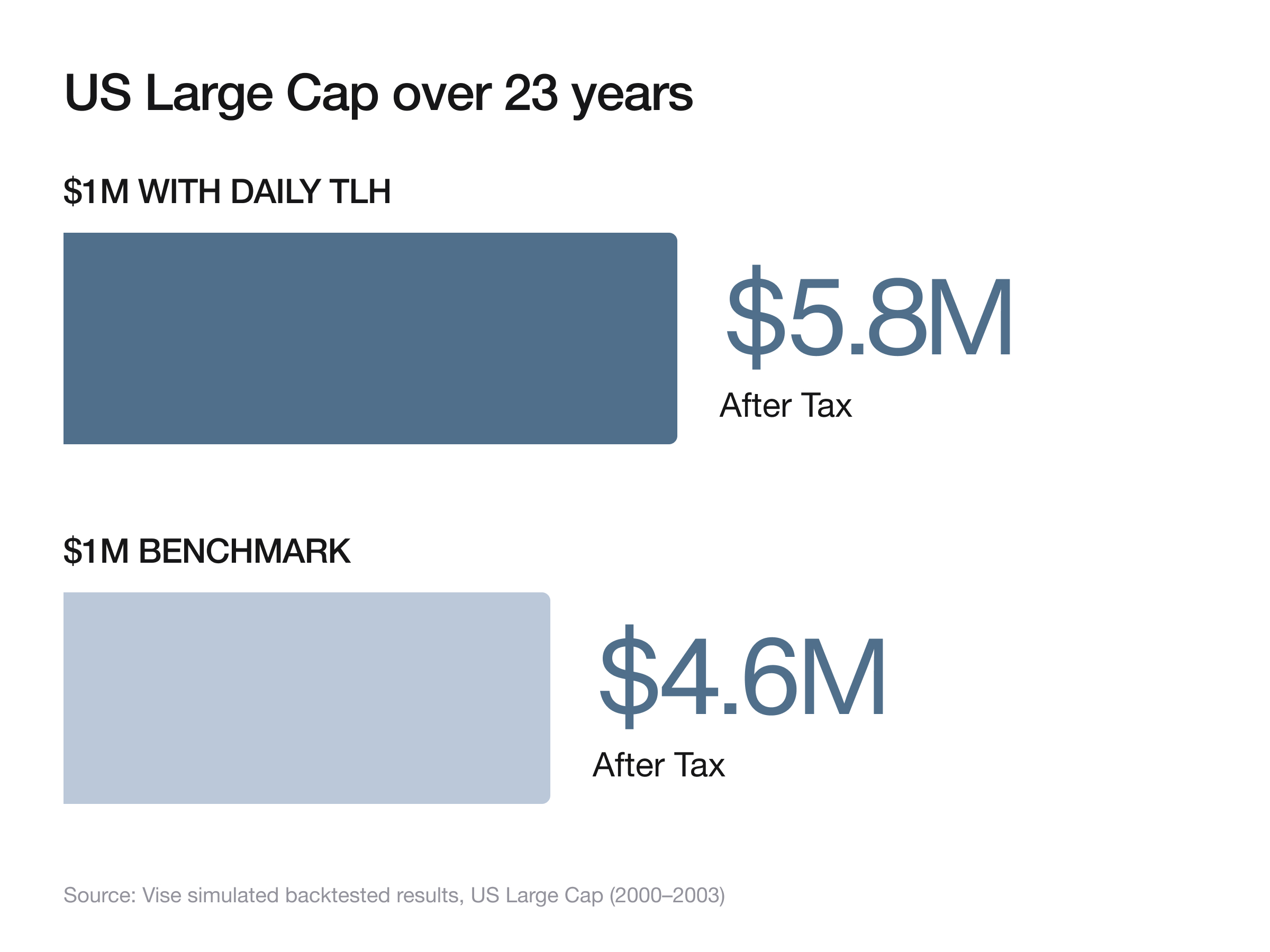

$1.2M in Extra Wealth from Tax Alpha Alone

The real power of daily harvesting shows up over time.

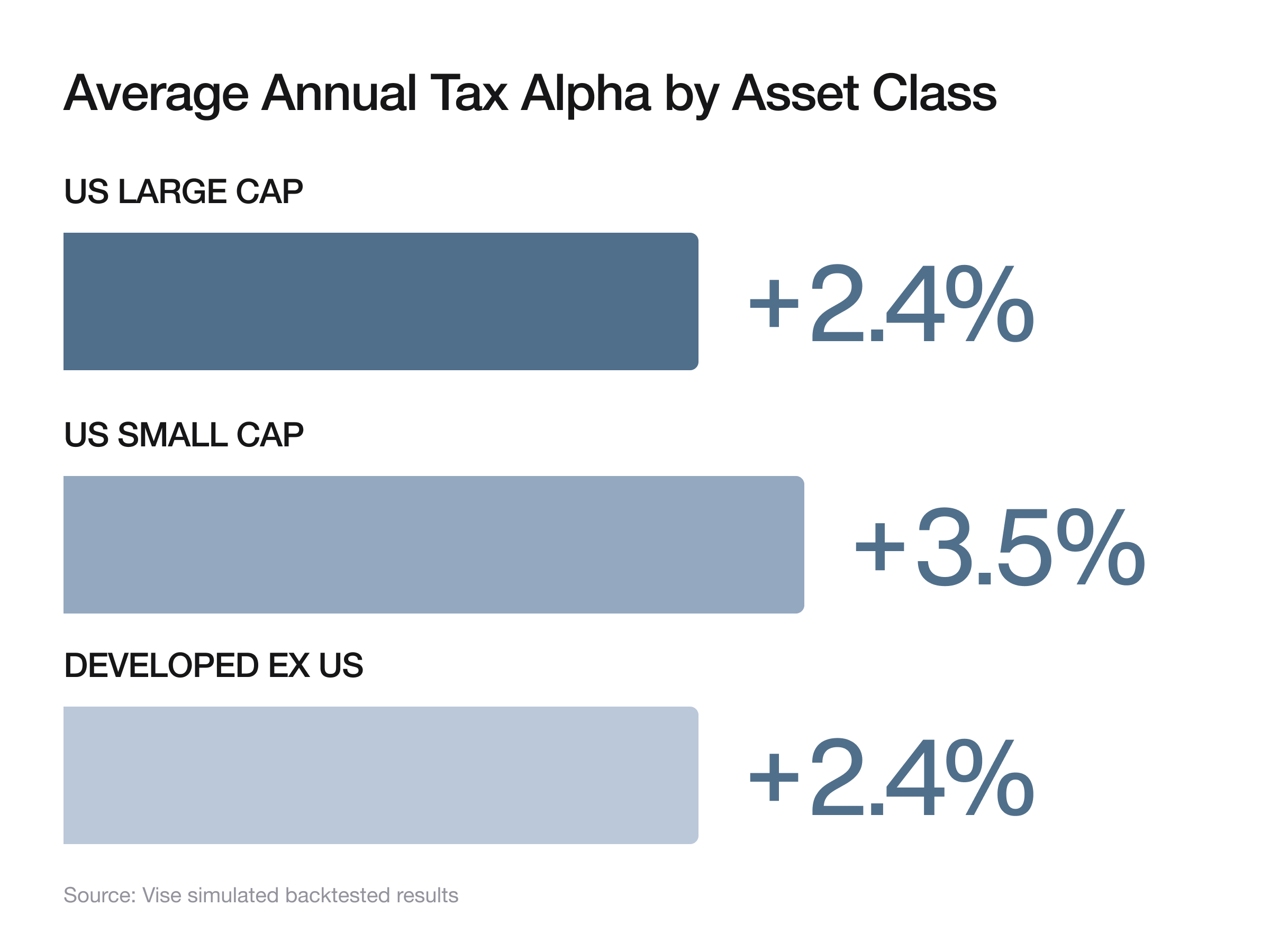

In US Large Cap, daily single-stock harvesting has generated an average of +3.0% annual tax alpha. Over 23 years, that has the potential to turn $1M into $5.8M after tax, compared to $4.6M for the benchmark after tax. That's $1.2M in additional portfolio value from tax alpha alone.2

In US Small Cap, the numbers are even more compelling: +3.5% average annual tax alpha. Small cap stocks are more volatile, which means more harvesting opportunities. More dispersion at the individual stock level means more chances to capture losses while the overall allocation stays on track.2

Even in Developed ex-US equities, where harvesting is done through US-listed ADRs, the strategy can add +2.1% in annual tax alpha, turning $1M into $2.4M versus $1.8M for the benchmark after tax.2

These aren't hypothetical improvements. They represent the structural advantage of looking at every position, every day, and acting when the math says to act.

Your ETF Can't Harvest What It Can't See

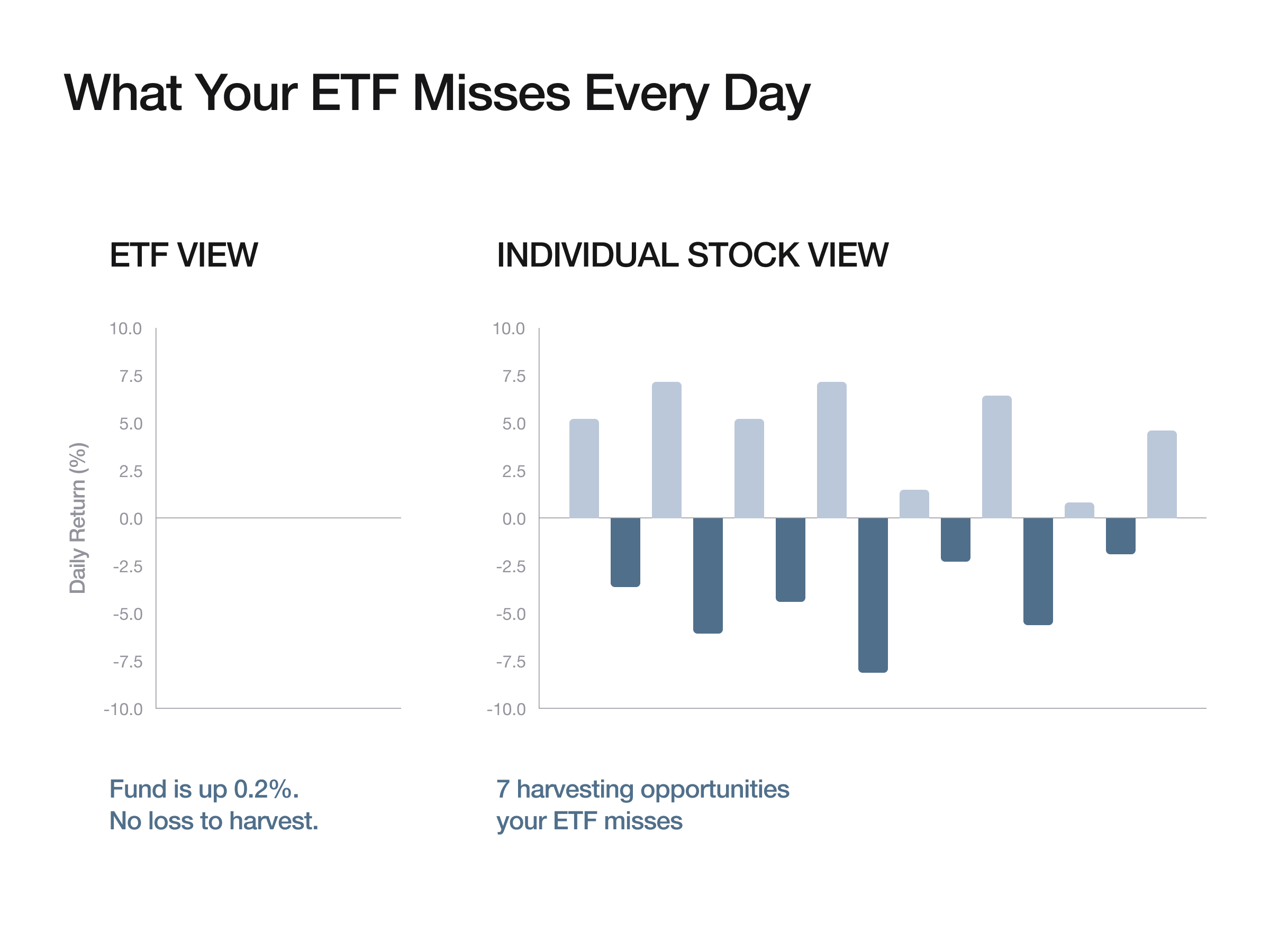

Most advisors who use tax-loss harvesting today do it at the ETF level: sell one fund, buy a similar one, capture the loss. It's simple, and it works to a point.

But ETF-level harvesting has a hard ceiling. You can only harvest a loss when the entire fund is down. Inside that fund, individual stocks are moving in different directions every day. Some are up 5%. Some are down 8%. At the fund level, those movements net out. At the individual stock level, every one of them is a potential harvesting opportunity.

That's the core insight behind direct indexing: unbundle the ETF, own the individual securities, and harvest losses at the position level. Daily single-stock harvesting can capture 3.10% in tax alpha versus 0.84% for annual ETF harvesting.1 As much as the vehicle matters, the frequency matters more.

The One Question Every Client Will Eventually Ask

Tax alpha is one of the few sources of consistent, repeatable value that advisors can deliver regardless of market conditions. You can't control returns. You can't predict the market. But you can systematically reduce your clients' tax burden every single day.

For a client in the top marginal bracket, every $10,000 in short-term losses harvested translates to $3,700 in tax savings.3 Multiply that across a diversified portfolio monitored daily, and the numbers compound fast.

This is especially powerful for high-net-worth clients with concentrated positions, significant capital gains from business sales or equity compensation, or complex tax situations where every basis point of tax efficiency matters. Daily harvesting doesn't just improve returns. It gives advisors a concrete, quantifiable answer to the question every client eventually asks: "What are you doing for me that I can't get somewhere else?"

Table Stakes Isn't Enough Anymore

The wealth management industry is converging on tax-loss harvesting as table stakes. The differentiator isn't whether you offer it. It's how well you execute it.

When every position in every portfolio is monitored and harvested automatically at the individual stock level, every single trading day, that combination has the potential to deliver nearly four times the tax alpha of the industry default. It compounds over years into meaningful, measurable differences in client wealth. And it gives advisors a value proposition that's difficult to replicate with quarterly spreadsheets or annual ETF swaps.

Across the Vise platform, we've generated $76M+ in total tax alpha for advisors and their clients.4 Not because the concept is new, but because the execution is relentless: every position, every portfolio, every day.

Sources

1 Tax-loss harvesting frequency data. Khang, Cummings, Paradise, and O'Connor. "Personalized Indexing: A Portfolio Construction Plan." Vanguard Research, March 2022. Figure 6 (Investor B: ultra-high-net-worth with unlimited loss-offsetting income). Results based on 10-year TLH strategies launched every January from 1982 to 2011, using the top 400 securities from the Axioma US4 risk model, with a 5% loss threshold and 10 bps per one-way transaction cost.

2 Asset class tax alpha performance. Vise simulated backtested results. US Large Cap and US Small Cap simulations use an inception date of June 2000; Developed ex-US (via US-listed ADRs tracking MSCI EAFE) uses an inception date of 2008. Tax alpha calculated by assuming net realized losses offset equivalent gains at a 37% short-term and 20% long-term marginal tax rate, with tax savings reinvested. Simulations are rebalanced monthly. These results are hypothetical, do not reflect actual client accounts, and are subject to backtesting limitations. Actual results vary based on starting portfolio, inception period, inflows/outflows, and individual client tax rates.

3 Tax savings calculation. Based on a 37% top federal marginal short-term capital gains tax rate applied to $10,000 in realized short-term losses ($10,000 x 37% = $3,700). Actual tax impact depends on individual circumstances. Consult a qualified tax professional.

4 $76M+ total tax alpha. Vise platform data as reported on vise.com.

Additional references: Chaudhuri, Burnham, and Lo. "An Empirical Evaluation of Tax-Loss-Harvesting Alpha." Financial Analysts Journal, 76(3), 2020. Khang, Paradise, and Dickson. "Tax-Loss Harvesting: An Individual Investor's Perspective." Financial Analysts Journal, 77(4), 2021.

Tax treatment is not guaranteed and may vary based on individual circumstances. Past performance, whether simulated or actual, is not indicative of future results. Consult with a qualified tax professional regarding your specific situation.